The Beginning of the End of ‘Free’

It always starts small.

First, it’s free.

Then it’s “nominal.”

Then, before you know it, it’s a new normal — and the middle class is footing the bill, again.

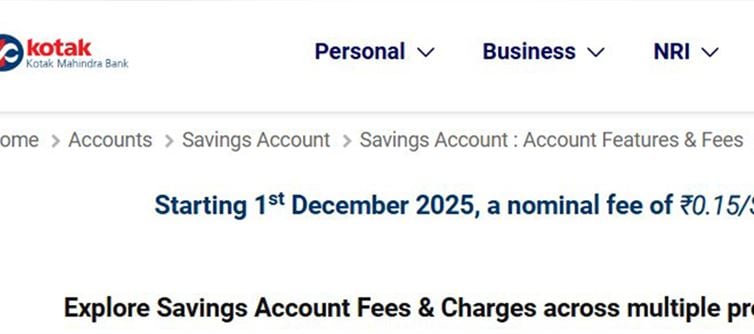

Kotak mahindra bank has announced a 15 paisa charge for every SMS alert.

Just 15 paisa, right? Not even the cost of a biscuit. But that’s the trick.

Because this isn’t about money — it’s about mindset.

Once one major player starts monetizing something as basic as a security alert, others will follow.

How the “Free Trap” Works

It’s a classic corporate playbook — time-tested, subtle, and cynical:

Offer a service for free. Let people rely on it.

Introduce a tiny fee. Call it “nominal.”

Increase it gradually. people won’t complain because it still “feels small.”

Normalize it across industries. Before long, everyone’s charging for what used to be free.

This is not innovation. It’s institutionalized conditioning.

We’ve seen it with ATM withdrawals, debit card renewals, cheque books, SMS alerts — and UPI might be next.

The 15 Paisa That Costs a Fortune

For a common man, SMS alerts are not a luxury.

They are a safety tool — a simple notification that prevents fraud, ensures awareness, and builds trust.

If banks start charging for every SMS, people will begin turning them off to save money — unknowingly making themselves more vulnerable to fraud and theft.

That’s not just unethical. That’s dangerous.

Banks were meant to make money management safer, not make security a paid feature.

The Death of Trust by a Thousand Cuts

We live in a time where every “convenience” is being rebranded as a subscription.

Need extra luggage on a flight? Pay.

Want to park your car in a mall? Pay.

Want an SMS from your own bank to tell you where your money went? Pay.

It’s not the 15 paisa that hurts.

It’s the slow transformation of banking from a service into a sales funnel.

The message is clear — you’re not a customer anymore; you’re a revenue stream.

Why the Middle Class Always Pays the Price

The ultra-rich don’t care. They have premium accounts with relationship managers.

The poor survive on Jan Dhan accounts with protections.

But the middle class — the silent, salaried, tax-paying majority — gets squeezed dry.

They pay for everything, question nothing, and receive nothing in return.

Every time a “minor charge” is introduced, they shrug and absorb it.

Because fighting the system feels pointless.

That’s how quiet exploitation works — not through theft, but through exhaustion.

The Domino Effect: From Banks to Everything Else

Make no mistake — once banks succeed with this model, others will follow.

Insurance companies, mutual funds, telecom providers — every sector watches what banks do.

If people accept paying for SMS alerts, it won’t be long before you’re charged for every update from your insurer, your demat account, or even your electricity bill.

Soon, every message that once protected you will become a micro-tax on your awareness.

The Dangerous Shift: From service to Monetization

There was a time when banks served the people.

Now, they serve profits.

They call it “digital transformation.”

But what it really is — a monetization of human trust.

When a customer signs up with a bank, they’re not buying a product — they’re entrusting their life savings.

And the least that the bank can do is tell them when money leaves their account without charging for the courtesy.

It’s Not About 15 Paisa — It’s About the Precedent

Today it’s 15 paisa.

Tomorrow it’ll be ₹1.

Next year, it’ll be ₹5.

And by then, it will be “industry standard.”

Remember how ATM withdrawals went from 5 free transactions to paid limits?

Remember how cheque books, SMS banking, debit card renewals — everything — slowly became “billable”?

That’s exactly how it happens.

Step by step. Paisa by paisa.

The Final Irony: Paying to Be Scammed

The cruelest twist in this entire story?

You’re now being charged to protect yourself from being robbed.

If you disable SMS alerts to avoid charges, you’ll lose visibility over every fraudulent or unauthorized transaction.

If you keep them on, you pay your bank for doing what it’s legally obligated to do — keep you informed.

You lose either way.

Final Word: The Cost of Silence

The issue isn’t the 15 paisa. It’s the precedent, the passivity, and the predictable silence.

Every new fee is tested quietly on customers.

If no one protests, it stays. If they do, it’s renamed, restructured, and reintroduced later.

The pattern is always the same — normalize, monetize, repeat.

Banks were meant to guard your wealth.

Now, they’re nibbling at it, one paisa at a time.

And unless people speak up now, soon every safety feature in your bank account will come with a price tag —

and you’ll be paying not for convenience,

but for the illusion of control.

click and follow Indiaherald WhatsApp channel

click and follow Indiaherald WhatsApp channel